Inflation and the coronavirus did not hold back the stock market last year, but in 2022, investors face new worries.

After a remarkably fruitful year in which the stock market shook off rising inflation and coronavirus cases, 2022 began with a decline. It may be the first in a series of ups and downs as Wall Street anticipates moves by the Federal Reserve and copes with the lingering pandemic.

It will be hard for investors to know what to do as the Delta variant gives way to Omicron and whatever variants evolve next. As for the Fed, the evolution of its policy is perplexing the markets, too. Recent statements and past behavior by its chair, Jerome Powell, suggest it will ramp up the effort to fight inflation, then change course if markets become unduly agitated.

“The markets have come to believe that if there’s a major correction in the equity market, Powell will help them out,” said Komal Sri-Kumar, president of Sri-Kumar Global Strategies. “The result is a seesaw motion in which the market corrects in anticipation of tightening, then the Fed eases and the market goes up.”

After the S&P 500 rose 10.6 percent in the fourth quarter, giving it a 26.9 percent gain for 2021, the index made a marginal new high as 2022 began, then lost ground.

One reason for the January decline is the release of minutes from the December Fed meeting, which showed growing discomfort about inflation and included discussion of accelerating the pace of interest rate increases. The minutes led some investment banks to forecast four rate increases this year instead of three and an earlier start to the process of selling the trillions of dollars of assets bought in the quantitative easing program.

But if inflation stays high after a period of tightening, Mr. Sri-Kumar said, the Fed will have to maintain that tighter policy, however sensitive the markets might be to it. Failure to do so could risk damaging the economy, he said, something the markets would be even more sensitive to.

Some investment advisers expect the Fed to become consistently hawkish. Bill Hester, senior research analyst at Hussman Strategic Advisors, said in a commentary on the firm’s website that Mr. Powell had made the case before the pandemic that forceful early action was required when inflation expectations threaten to get out of control.

The Fed may be closer to making that determination than many realize, Mr. Hester said. The unemployment rate, 3.9 percent according to December data reported this month, is lower than in 2015, at the start of a Fed tightening cycle during which the labor market continued to strengthen. Moreover, the labor force has been shrinking as fewer people are working or seeking work, which might encourage the Fed to think that full employment can be achieved with a higher unemployment rate.

There is also a benign possibility, which Rick Rieder, head of the global asset allocation team at BlackRock, adheres to, in which inflation ebbs on its own.

“Some tangible changes will kick in, in the second or third quarter,” he said. “Inventory levels are in really good shape” on many goods, “and we should see some alleviation of pressure on energy prices.” Also helping is that consumer price comparisons with a year earlier will be more favorable.

Simeon Hyman, global investment strategist at ProShares, an issuer of exchange-traded funds, is another inflation optimist. He expects Fed tightening to succeed, and he highlighted snippets of data, such as a recent steep drop in the Baltic Dry Index, which measures global shipping rates, to back his case. He anticipates inflation falling to 3 percent, “a number that stocks can digest,” and forecasts S&P 500 earnings to rise 10 percent to 15 percent this year, “enough for stocks to do OK.”

Stocks did better than OK last year. The average domestic stock fund tracked by Morningstar rose 6.6 percent in the fourth quarter and 21.9 percent on the year, although both results lagged the S&P 500 considerably.

A handful of giant technology stocks accounted for much of the market’s return, but tech funds performed only in line with broad stock portfolios. Many of the best sector funds focused on financial services and natural resources.

International stock funds had an ordinary year, rising 7.9 percent, including 1.9 percent in the fourth quarter. There were vast differences in results geographically, with specialists in Europe and India greatly outperforming and Latin America and China funds showing losses.

Mutual Funds

Highlights of mutual fund performance in the second quarter.

Leaders and Laggards

Stocks vs. Bonds

Among general domestic stock funds.

Average returns, by fund category.

12 MONTHS

2ND QTR.

LEADERS

12 MONTHS

2ND QTR.

+

+

+

+

44.2

35.8

6.5

5.4

%

+

+

+

+

6.7

5.7

1.8

1.8

%

Edgewood Growth

Institutional

+

+

+

+

+

+

+

+

48.3

77.3

42.3

40.1

79.1

60.1

44.4

42.5

%

+

+

+

+

+

+

+

+

18.1

17.1

16.1

16.0

15.4

15.1

14.8

14.8

%

General stock funds

International stocks

Aegis

Value I

Taxable bonds

Franklin Growth

Opportunities R6

Municipal bonds

TCW Select

Equities I

Growth vs. Value

Returns in the second quarter.

Baillie Gifford US

Equity Growth K

Growth

Blend

Value

+

10

%

Morgan Stanley

Inst. Growth IR

+

8

+

6

Franklin Focused

Growth A

+

4

Principal Blue

Chip R-6

+

2

0

Large-cap

MiDcap

Small-cap

Sector by Sector

12 MONTHS

2ND QTR.

LAGGARDS

12 MONTHS

2ND QTR.

Industrials

+

+

+

+

+

+

+

+

+

+

52.7

35.3

51.4

41.0

62.6

22.3

67.4

28.5

46.0

17.9

%

+

+

+

+

+

+

+

+

+

+

12.0

11.6

9.9

9.2

7.9

6.5

4.1

3.6

2.6

0.9

%

Towle

Deep Value

+

+

+

+

+

+

+

+

88.7

61.5

89.7

50.3

52.0

33.4

108.9

77.6

%

–

–

–

–

–

–

–

–

1.0

1.1

1.5

1.6

1.7

2.2

5.6

6.4

%

Real estate

SouthernSun

Small-Cap, I

Technology

Kinetics Paradigm

Adv C

Communications

Harbor Small-Cap

Value Investor

Natural resources

Health

Fairholme

–

+

–

+

Financial

Delaware Ivy

ProShrsRusl2000

Consumer defensive

Jacob Discovery

Fd Inv

Energy

Utilities

Kinetics Market

Opp. No Load

Stocks vs. Bonds

Average returns, by fund category.

12 MONTHS

2ND QTR.

+

+

+

+

44.2

35.8

6.5

5.4

%

+

+

+

+

6.7

5.7

1.8

1.8

%

General stock funds

International stocks

Taxable bonds

Municipal bonds

Growth vs. Value

Returns in the second quarter.

Growth

Blend

Value

+

10

%

+

8

+

6

+

4

+

2

0

Large-cap

MiDcap

Small-cap

Sector by Sector

12 MONTHS

2ND QTR.

Industrials

+

+

+

+

+

+

+

+

+

+

52.7

35.3

51.4

41.0

62.6

22.3

67.4

28.5

46.0

17.9

%

+

+

+

+

+

+

+

+

+

+

12.0

11.6

9.9

9.2

7.9

6.5

4.1

3.6

2.6

0.9

%

Real estate

Technology

Communications

Natural resources

Health

Financial

Consumer defensive

Energy

Utilities

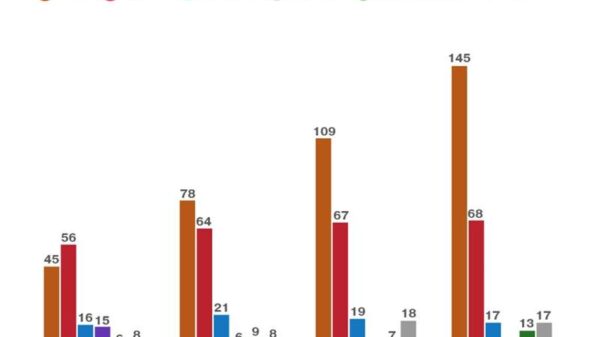

Leaders and Laggards

Among general domestic stock funds.

LEADERS

12 MONTHS

2ND QTR.

Edgewood Growth

Institutional

+

+

+

+

+

+

+

+

48.3

77.3

42.3

40.1

79.1

60.1

44.4

42.5

%

+

+

+

+

+

+

+

+

18.1

17.1

16.1

16.0

15.4

15.1

14.8

14.8

%

Aegis

Value I

Franklin Growth

Opportunities R6

TCW Select

Equities I

Baillie Gifford US

Equity Growth K

Morgan Stanley

Inst. Growth IR

Franklin Focused

Growth A

Principal Blue

Chip R-6

12 MONTHS

2ND QTR.

LAGGARDS

+

+

+

+

+

+

+

+

88.7

61.5

89.7

50.3

52.0

33.4

108.9

77.6

%

–

–

–

–

–

–

–

–

1.0

1.1

1.5

1.6

1.7

2.2

5.6

6.4

%

Towle

Deep Value

SouthernSun

Small-Cap, I

Kinetics Paradigm

Adv C

Harbor Small-Cap

Value Investor

–

+

–

+

Fairholme

Delaware Ivy

ProShrsRusl2000

Jacob Discovery

Fd Inv

Kinetics Market

Opp. No Load

Stocks vs. Bonds

Average returns, by fund category.

12 MONTHS

2ND QTR.

+

+

+

+

44.2

35.8

6.5

5.4

%

+

+

+

+

6.7

5.7

1.8

1.8

%

General stock funds

International stocks

Taxable bonds

Municipal bonds

Growth vs. Value

Returns in the second quarter.

Growth

Blend

Value

+

10

%

+

8

+

6

+

4

+

2

0

Large-cap

MiDcap

Small-cap

Sector by Sector

12 MONTHS

2ND QTR.

Industrials

+

+

+

+

+

+

+

+

+

+

52.7

35.3

51.4

41.0

62.6

22.3

67.4

28.5

46.0

17.9

%

+

+

+

+

+

+

+

+

+

+

12.0

11.6

9.9

9.2

7.9

6.5

4.1

3.6

2.6

0.9

%

Real estate

Technology

Communications

Natural resources

Health

Financial

Consumer defensive

Energy

Utilities

Leaders and Laggards

Among general domestic stock funds.

LEADERS

12 MONTHS

2ND QTR.

Edgewood Growth

Institutional

+

+

+

+

+

+

+

+

48.3

77.3

42.3

40.1

79.1

60.1

44.4

42.5

%

+

+

+

+

+

+

+

+

18.1

17.1

16.1

16.0

15.4

15.1

14.8

14.8

%

Aegis

Value I

Franklin Growth

Opportunities R6

TCW Select

Equities I

Baillie Gifford US

Equity Growth K

Morgan Stanley

Inst. Growth IR

Franklin Focused

Growth A

Principal Blue

Chip R-6

12 MONTHS

2ND QTR.

LAGGARDS

+

+

+

+

+

+

+

+

88.7

61.5

89.7

50.3

52.0

33.4

108.9

77.6

%

–

–

–

–

–

–

–

–

1.0

1.1

1.5

1.6

1.7

2.2

5.6

6.4

%

Towle

Deep Value

SouthernSun

Small-Cap, I

Kinetics Paradigm

Adv C

Harbor Small-Cap

Value Investor

–

+

–

+

Fairholme

Delaware Ivy

ProShrsRusl2000

Jacob Discovery

Fd Inv

Kinetics Market

Opp. No Load

Much of how 2022 unfolds will depend on the coronavirus and the response to it. If evidence continues to pile up that Omicron is more transmissible than other variants, but milder, it could show the way out of the pandemic. That could be great for society but potentially harmful for investors by removing the virus as a deus ex machina that has helped to make market conditions ideal.

In response to the coronavirus, the Fed created trillions of dollars out of thin air, Congress doled out trillions more, and the pandemic provided a tacit guarantee that interest rates wouldn’t rise. If Omicron means a return to regular order, investors will have to contend with the highest inflation in a generation, record fiscal debt and a Fed lacking a reason not to tackle inflation forcefully. At the same time, stocks and bonds are very expensive, limiting prudent investment options.

“There’s no place to hide,” Melda Mergen, global head of equities at Columbia Threadneedle Investments, said during a presentation of the firm’s 2022 outlook. “Most of the markets are at the top of the bar in their current valuations.”

She remains bullish toward stocks but emphasizes pockets that are less expensive, such as smaller companies and value stocks. She noted, though, that the valuation gap between growth and value stocks has narrowed, so the pickings are slimmer.

Other investment advisers also recommend looking for less overpriced market segments, but they differ on where to find them. Mr. Sri-Kumar likes European stocks more than American ones, and he would buy emerging markets, such as India, that do not depend on strong growth in China, where he foresees growing risk in 2022.

Ian Mortimer, a co-manager of the Guinness Atkinson Global Innovators fund, suggests owning “quality defensives,” stocks in industries that feature rising dividends. Some examples are British American Tobacco, Imperial Brands, which also sells tobacco, and the insurance company Aflac.

For Mr. Hyman, “the view for stocks is a lot better than the view for bonds.” He said the financial, energy and materials industries tend to do well when interest rates rise.

If stocks do better than bonds in 2022, it will mean more of the same for fund owners. The average bond fund was flat in the fourth quarter and up 1 percent for all of 2021. The standout niches, each returning about 5 percent on the year, held bank loans and high-yield bonds.

Mr. Rieder favors such diverse assets as carmakers’ shares, investment-grade corporate bonds, and stocks in Indonesia and Colombia, although he broadly prefers American markets to foreign ones. He predicts low-double-digit gains for the S&P 500.

But he tempers his optimism with concern that inflation might not abate and that the Fed has instilled “a sense of complacency in the markets.”

“That’s going to make their job a lot harder from here,” he said, adding, “If they waited too long and have to brake hard on the other side, it will cause the markets to go down hard.”